'%3e %3cpath d='M15.9571 0.231934L0.147583 9.39139V32.66L15.9571 41.8195L31.7665 32.66V9.39139L15.9571 0.231934ZM15.9571 33.0172L7.68318 28.2206V13.7798L15.9571 9.00869V23.424L24.2309 28.2206L15.9571 33.0172Z' fill='%23170E30'/%3e %3cpath d='M107.275 23.3727C107.275 22.9645 107.275 22.6073 107.275 22.2756C107.275 21.6377 107.021 20.311 106.766 19.7242C104.628 14.6214 96.3791 15.5144 95.5645 21.3316C94.648 28.0417 102.438 30.9248 106.613 26.2302L104.678 24.929C102.464 26.8936 98.9759 26.5619 98.2885 23.3982H106.384H107.275V23.3727ZM98.2885 21.3826C99.0268 17.9382 103.966 17.7596 104.449 21.3826H98.2885ZM58.472 16.5095C53.9914 15.7441 51.1147 19.1629 51.522 23.4492C51.9802 28.0672 57.8865 30.2614 61.0688 26.766V28.1438H63.9964V16.3309C63.9964 16.3309 61.1706 17.9638 61.0433 18.0403C61.0433 18.0403 59.7959 16.7391 58.472 16.5095ZM57.3264 25.822C53.5077 25.3883 53.5332 19.6987 57.0464 19.1119C62.469 18.1934 62.5963 26.4088 57.3264 25.822ZM126.929 25.4648C126.471 29.5981 118.197 29.3429 116.924 25.6944L119.011 24.4698C119.597 26.1537 122.881 27.1487 123.95 25.6944C125.274 23.9085 121.048 23.4747 120.055 23.092C118.91 22.6328 117.586 21.8419 117.408 20.5151C116.72 15.5655 124.765 14.9786 126.623 18.6781L124.689 19.8263C124.103 18.2954 120.157 17.479 120.284 19.6222C120.361 20.8468 123.517 21.204 124.561 21.6633C126.318 22.4287 127.132 23.4747 126.929 25.4648ZM90.5492 18.2954C87.2142 14.3918 81.3334 16.8667 80.8497 21.7908C80.3151 27.4294 86.5523 30.8993 90.5238 26.6129V28.1438H93.2987V12.1211H90.5238V18.2699L90.5492 18.2954ZM87.7998 25.7965C83.1409 26.5874 82.2499 19.7497 86.4759 19.0864C91.2366 18.3465 92.0003 25.0566 87.7998 25.7965ZM75.8599 18.2954L74.918 17.3004C70.0555 14.3408 65.0657 19.0098 66.4404 24.2402C67.4333 28.0162 72.2958 29.9808 75.3253 27.2253C75.5544 27.0212 75.6053 26.6895 75.8599 26.6129V28.1438H78.6348V12.1211H75.8599V18.2699V18.2954ZM73.1104 25.7965C68.3752 26.4854 67.7897 19.7497 71.8121 19.1119C76.7 18.321 77.311 25.2097 73.1104 25.7965ZM112.392 16.6115H109.465V28.1693H112.392V21.102L115.6 19.2394V16.3054C114.709 16.8156 112.876 17.8872 112.392 18.1679V16.6115ZM42.4335 25.3883H49.969V28.1693H39.353V13.7795H42.4335V25.3883Z' fill='%23170E30'/%3e %3c/g%3e %3cdefs%3e %3cclipPath id='clip0_1_15718'%3e %3crect width='127' height='42' fill='white'/%3e %3c/clipPath%3e %3c/defs%3e %3c/svg%3e)

I’m waking up every damn morning with a smile on my face with the following 18-or-so hours ahead of me to do with as I please. The other 6 hours or so I’m sleeping. I’ve found I don’t need a ton of sleep.

I have no bosses to impress, no time cards to punch and no stupid deadlines or endless meetings just for the sake of “team unity”. In early retirement, you truly are the master of your domain.

Follow Ladders on Flipboard!

Follow Ladders’ magazines on Flipboard covering Happiness, Productivity, Job Satisfaction, Neuroscience, and more!

But, it won’t always be quite as easy for everyone, and it all starts with a very simple and unifying theme:

You need to do something in early retirement – that’s your purpose

I can talk about purpose until I’m blue in the face because, well, it really is that important. Not that I relish the thought of losing enough oxygen for my face to get blue, but you get the idea.

Purpose is kinda important.

It’s important because having the entire day ahead of you with nothing on the schedule comes with it a whole other set of potential problems. When the buck stops with you, shit gets real.

Do you want shit to get real? I mean, that real? Do you want the responsibility of owning your entire day without the structure that a full-time job often provides?

It’s similar to “being your own boss” or working for yourself. It sounds good in theory, but you also need to own it. You need to be a special kind of person to manage yourself.

It’s not as easy as it sounds.

To successfully manage your own time in early retirement, you need to know yourself…well. You need to know what makes you happy and what doesn’t. You need to balance your fun with your “work” and know how much time to devote to each individual thing.

If you think that’s easy, then you might be in for a world of hurt.

On the flip side, you can’t over-schedule yourself after quitting your job

I have fallen terribly close to this point in early retirement. I’m so motivated to try new things and get involved that, quite frankly, I have a tough time saying no. I’m always looking for more.

And, that’s not always a good thing.

For instance, I have this huge blog that I’m maintaining. My wife and I also run a growing YouTube channel at A Streamin’ Life. What else?

- I started another blog about digital marketing

- I do consulting work at Rockstar Finance

- I write for bloggers/websites on specific projects

- I’m involved in several blog projects

- And, my wife and I travel the country for a living

All this stuff takes time, and I’d be lying if I said that time never gets away from me. Even after retiring early, I sometimes feel that there aren’t enough hours in the day, and that’s my own fault.

I just like being involved with things. Things that keep me focused and energized. Ultimately, a strongly believe that’s good. It is.

But, the trick is to properly manage your time so you don’t feel like you have a job again. After all, I retired early in large part to recapture my time, and the last thing that I want to do is sign myself up for enough projects that I feel like I don’t have enough time to just…relax and enjoy life.

Managing your time is crucial.

You’ll fail without time-management

Forget the money component of early retirement for a minute. Of course, we all know that we need money before quitting our jobs. That’s the most obviously and clear-cut aspect of #FIRE.

What isn’t so clear-cut is, well, us. You and me.

Life is an organic entity. We aren’t using a bunch of repeatable mathematical equations to rule our time like we might use to come up with how much money we’ll need before calling it quits.

If you can’t manage your time, you won’t be happy in early retirement. It really is that simple. You can’t quit your work structure if you can’t replicate that with a better structure.

It’s a structure that you design and impose upon yourself. This is the hard part.

And, I cannot teach you how to do this, but I can give you the basic outline of what a solid structure looks like.

- What times of the day do you feel most productive?

- Are you an early morning person or a late riser?

- Are your hobbies easy enough to pursue on a daily basis?

- Do you have a one year, two years and five-year goals?

A direction is critical, and understanding how you work the best is how to set yourself up on the path to head that way.

For example, I know that I do my best work in the morning hours. Therefore, I focus on the most critical aspects of my life in the morning. Everything else takes second priority. The morning is my time to focus.

When I can properly focus, I can get my “work” done on my side projects. I feel productive and motivated to repeat that process the next day and I’m actively strutting in the direction that I need to go.

The more that you understand about yourself, the better equipped you’ll be to customize your life in a way that makes sense.

Stop worrying about the damn risks

First, let me preface this discussion with a very simple statement: Anything can happen in early retirement. You might fall down a flight of stairs the day after you call it quits, break your leg and undergo a series of painful and expensive surgeries.

Or, you might get into a car accident. Or a train wreck. Or contract a disease. Or…*fill in the blank*. The point is that yes, things happen. Markets crash. People over-spend.

There’s no doubt that quitting your full-time source of income in your 30s, and expecting to live not 20, 30, or even 40 more years…try, 60 or 70, without a dedicated income for more than half of your life, is a risk.

But for most of us, it’s a calculated risk. But, here’s an important question that we need to ask ourselves.

What about the risks of staying at our jobs? – especially stressful ones. As ABC reports: “A growing body of research stands testament to this fact: lack of sleep has been shown to tax the hearts of the stressed executive and the stressed day worker alike.

“Layoffs,” the report continues, “can take their psychic and physiologic toll in the executive suite and on the production line; the burden on those left behind, who work more overtime to shoulder a heavier workload, can be life-shortening; and living in fear of losing a job, or staying put in a hostile workplace, also boosts the risk of an earlier cardiac death.”

I hate the risk of not retiring early more than the opposite. To work the vast majority of our life and then retire during the portion of our life where we’re more likely to get sick is a dreadful thought. To develop cancer. Suffer from mobility-inhibiting aches and pains. It’s painful to even think about.

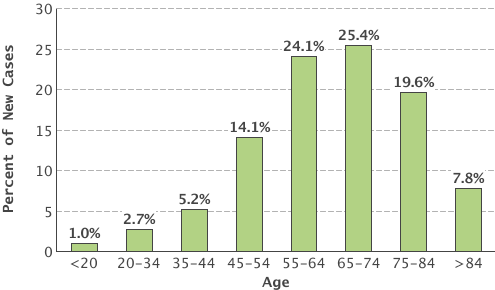

Consider this graph from Cancer.gov. The wide majority who develop cancer are above the age of 50.

The highest incidents of cancer occur between 65 and 74 which, coincidently, happens to coincide closely with the age that we can draw social security without penalty: 62.

Does anyone else see a problem with this?

Risks run in both directions, ladies and gentlemen. We’re wise not to hone in on the risks OF early retirement and ignore the risks of NOT taking your life (and your time) into your own hands.

To me, it’s way more risky to retire during the period when we’re most likely to develop a health problem than it is much earlier in life.

At what point do we begin to consider the risks of NOT retiring early and weigh those against the risks of quitting the rat race early?

Risk is a two-way street, my friends.

Every once in a while, do something insane

I’ve written about this one before: Comfort zones crush our ability to improve our lives. They keep us wrapped up in a cocoon of mush, complacent and completely relaxed. Reflection and bettering our lives is often the furthest thing from our minds when we’re in these zones.

Instead of going to the gym to begin that new fitness program, we give ourselves an excuse to stay home. Rather than dropping by the neighborhood pot luck to meet the neighbors and network, we catch the latest episode of [insert popular TV sitcom here because I honestly have no idea].

It is natural to want comfort. And occasionally, there’s nothing wrong with a little time in our comfort zones. But spending too much time in this zone is detrimental to our progress. Get out of it.

Remember that time that we gave a speech about financial independence in front of hundreds of people? I do, because that was just a couple of months ago at the RV Entrepreneur Summit.

Okay, while I wouldn’t consider that “insane”, it definitely got us out of our comfort zones. We were nervous as hell before going up there, but once we got up on stage, everything fell right into place.

Confidence is a convenient virtue

I am, like, super duper confident. Confident to a fault.

I firmly believe that what we are doing is the absolute right thing, and we’ve made our decision. We are jumping in head first and not looking back. I quit a high paying and relatively low-stress job in the Information Technology industry for a life of freedom.

And I’m damn proud of what we’re doing.

Confidence is very different than arrogance. I don’t believe that I’m “always right”. I believe that I make the very best decisions that I can base on the information I have at the time. If I’m wrong, then I’m wrong. Big deal.

We fix it and move on.

Life sucks when we spend it second-guessing ourselves. So, I don’t. I believe that things will work out. I know that we are flexible and will roll with the punches.

I’m not worried about health care (gasp!). I don’t care who our president is. I refuse to let external factors that I cannot control dictate my life. The only thing that I can control is me. My life. My reactions. My motivations.

Confidence is key to keeping a sound mind and determined future. The more confident you are, the better prepared you’ll be to make early retirement work. Why?

Because early retirement, just like life, is a mind game. If you win the battle inside your head, you’ll win the battle outside of it as well.

What does financial independence and early retirement actually mean to you?

For me, financial independence is simple: it means that you are not beholden to a job to provide for your livelihood.

Instead, your wealth – acquired through a high level of income or aggressive savings plan, supports your lifestyle. While you may still work, you don’t need to. You work because you enjoy it.

To my wife, financial independence is a choice. It refers to the ability to choose the life that we all desire and live it as the person that we all choose to be.

Whatever it means to you, make sure that you understand it. This is your guiding principle that’ll help ensure you’re on the straight and narrow.

This article originally appeared on ThinkSaveRetire.

You might also enjoy…

- New neuroscience reveals 4 rituals that will make you happy

- Strangers know your social class in the first seven words you say, study finds

- 10 lessons from Benjamin Franklin’s daily schedule that will double your productivity

- The worst mistakes you can make in an interview, according to 12 CEOs

- 10 habits of mentally strong people