'%3e %3cpath d='M15.9571 0.231934L0.147583 9.39139V32.66L15.9571 41.8195L31.7665 32.66V9.39139L15.9571 0.231934ZM15.9571 33.0172L7.68318 28.2206V13.7798L15.9571 9.00869V23.424L24.2309 28.2206L15.9571 33.0172Z' fill='%23170E30'/%3e %3cpath d='M107.275 23.3727C107.275 22.9645 107.275 22.6073 107.275 22.2756C107.275 21.6377 107.021 20.311 106.766 19.7242C104.628 14.6214 96.3791 15.5144 95.5645 21.3316C94.648 28.0417 102.438 30.9248 106.613 26.2302L104.678 24.929C102.464 26.8936 98.9759 26.5619 98.2885 23.3982H106.384H107.275V23.3727ZM98.2885 21.3826C99.0268 17.9382 103.966 17.7596 104.449 21.3826H98.2885ZM58.472 16.5095C53.9914 15.7441 51.1147 19.1629 51.522 23.4492C51.9802 28.0672 57.8865 30.2614 61.0688 26.766V28.1438H63.9964V16.3309C63.9964 16.3309 61.1706 17.9638 61.0433 18.0403C61.0433 18.0403 59.7959 16.7391 58.472 16.5095ZM57.3264 25.822C53.5077 25.3883 53.5332 19.6987 57.0464 19.1119C62.469 18.1934 62.5963 26.4088 57.3264 25.822ZM126.929 25.4648C126.471 29.5981 118.197 29.3429 116.924 25.6944L119.011 24.4698C119.597 26.1537 122.881 27.1487 123.95 25.6944C125.274 23.9085 121.048 23.4747 120.055 23.092C118.91 22.6328 117.586 21.8419 117.408 20.5151C116.72 15.5655 124.765 14.9786 126.623 18.6781L124.689 19.8263C124.103 18.2954 120.157 17.479 120.284 19.6222C120.361 20.8468 123.517 21.204 124.561 21.6633C126.318 22.4287 127.132 23.4747 126.929 25.4648ZM90.5492 18.2954C87.2142 14.3918 81.3334 16.8667 80.8497 21.7908C80.3151 27.4294 86.5523 30.8993 90.5238 26.6129V28.1438H93.2987V12.1211H90.5238V18.2699L90.5492 18.2954ZM87.7998 25.7965C83.1409 26.5874 82.2499 19.7497 86.4759 19.0864C91.2366 18.3465 92.0003 25.0566 87.7998 25.7965ZM75.8599 18.2954L74.918 17.3004C70.0555 14.3408 65.0657 19.0098 66.4404 24.2402C67.4333 28.0162 72.2958 29.9808 75.3253 27.2253C75.5544 27.0212 75.6053 26.6895 75.8599 26.6129V28.1438H78.6348V12.1211H75.8599V18.2699V18.2954ZM73.1104 25.7965C68.3752 26.4854 67.7897 19.7497 71.8121 19.1119C76.7 18.321 77.311 25.2097 73.1104 25.7965ZM112.392 16.6115H109.465V28.1693H112.392V21.102L115.6 19.2394V16.3054C114.709 16.8156 112.876 17.8872 112.392 18.1679V16.6115ZM42.4335 25.3883H49.969V28.1693H39.353V13.7795H42.4335V25.3883Z' fill='%23170E30'/%3e %3c/g%3e %3cdefs%3e %3cclipPath id='clip0_1_15718'%3e %3crect width='127' height='42' fill='white'/%3e %3c/clipPath%3e %3c/defs%3e %3c/svg%3e)

American household debt hit a record $3 trillion dollars last year, shared between 300 million borrowers. The breed and extent of debt segmented amongst this demographic is principally beholden to age. According to the latest Survey of Consumer Finances report, the breakdown is as follows:

Under 35: $67,400

35–44: $133,100

45–54: $134,600

55–64: $108,300

65–74: $66,000

75 and up: $34,500

Follow Ladders on Flipboard!

Follow Ladders’ magazines on Flipboard covering Happiness, Productivity, Job Satisfaction, Neuroscience, and more!

Students loans and credit debt make of the majority of debt facing millennials. A recent Sofi survey reports that 83% of millennials feel that their student loan debt is keeping them from sleeping at night. A Bank of America survey published this year of 1,000 Americans found that 51% are worried about their finances- a worry energized by the fear of not having enough savings, the threat of a looming recession, and a perceived inability to mitigate their deepening debt.

Money, being such a structural part of any functioning society, has exceeded its right to govern class barriers, and has increasingly gained more ground in our collective psyche.

The psychology of debt

The Ascent Staff just released a new report surveying over 1,000 indebted Americans in an attempt to unpick the correlation between happiness, fulfillment, self-esteem, and financial distress. The authors report, “Of our respondents, 523 were female, 482 were male, and two did not identify as male or female. Our average respondent was 37 years old. To ensure that all respondents took our survey, all were required to identify and pass a carefully disguised attention-check question.”

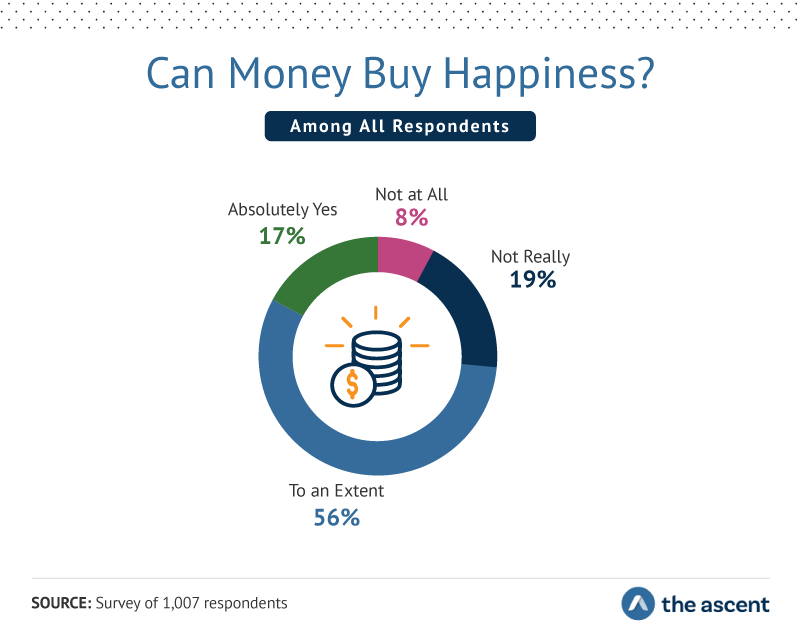

Consumer debt has been surging for 17 consecutive quarters. With this in mind, the researchers began their query by discerning a potential cause, a mindset that might be ensuring these numbers keep rising in spite of the lurid results. It may very well be that a misguided association with money and well being might cow under-employed Americans to splurge beyond their means. So the experts posed the age-old question to their study group: “Can money buy happiness?”

Fifty-six percent of the respondents involved in the study said “to an extent,” 19% said “not really,” 17% said “absolutely yes,” and a modest 8% said, “not at all.”

Previously conducted research favors the respondents that offered a sober yes as it turns out. It should be noted that even though there was some ambivalence surrounding the key question: Can money buy happiness?” The majority of respondents (63%) believed that wealthy people were indeed happier than people of lower income. This estimation is likely conditioned towards improvised or oppressed individuals that come into financial security later in life.

A study conducted on residents in rural Zambia found that women who received monthly money transfers exhibited a boost to overall well-being, specifically as it related to their children’s mental state, health, and future prospects.

Most of the respondents in the new study seemed to demarcate financial status with debt in particular, perceiving the latter much more bleakly. Ninety-seven percent of respondents said they would be happier if they were free of their debt. Forty-eight percent believed that their debt hindered their optimism, 47% felt that their debt adversely impacted their self-esteem, and an additional 43% reported debt affecting their sense of direction. In a less philosophical sense, the majority of respondents agreed that their debt made it harder for them to save money for their future, occasionally treat themselves, live their desired lifestyle, pursue their passions and interests and donate to important charities and causes.

All of these toxic factors coalesce into one giant mass, occupying the greater half of the American psychosis. Seventy-one percent of respondents said that they think about debt a lot more than they’d like to, which leads many to submit to relentless shame and self-loathing. Forty-percent of people with debt has either lied or actively hid it from others at least once.

Good and bad debt

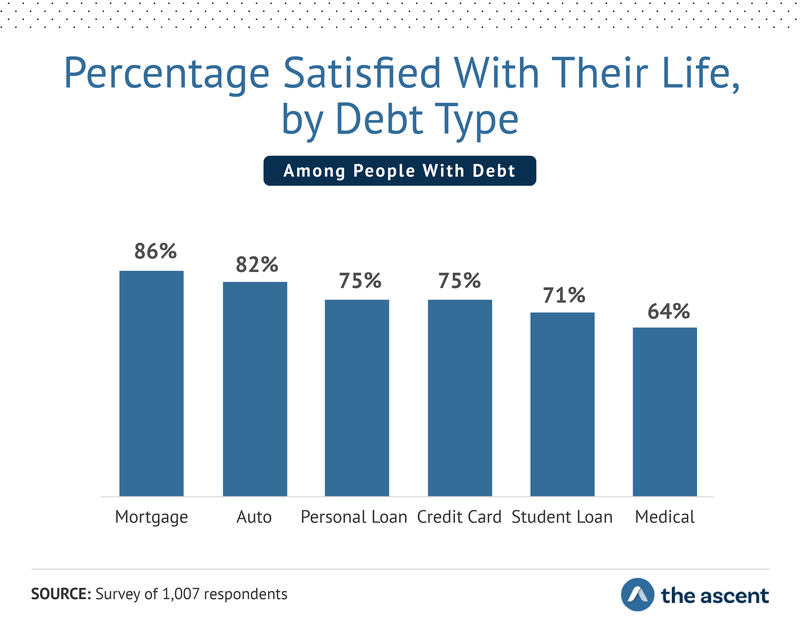

Different kinds of debt seemed to carry different degrees of stress and anxiety. After all, there is such a thing as “good debt.” Good debt is defined as a calculated investment that is expected to grow in value, generate income or provide some kind of comfort at some point in the future. It thus stands to reason that those with mortgages, which serves as a standard of good debt as you could conceive, proved to be the most satisfied of all the debt holders studied.

Interestingly enough, however, the other classic good debt exemplar, student loans, yielded some of the least satisfied participants, coming second only to people with medical loans. Medical debt was the only category that housed a healthy percentage of people being unable to make the minimum amount of payments, as 42% expressed being unable to do so.

In regards to the ignominy brought on by debt, the authors conclude, “If you’re in debt, it can feel overwhelming — like you’re carrying the weight of your loans on your shoulders, metered out in gold bars. Whenever your mind ends up wandering to dark places, just remember that debt is ageless, faceless, and genderless: Hundreds of millions of Americans are currently walking around with some form of debt.”