'%3e %3cpath d='M15.9571 0.231934L0.147583 9.39139V32.66L15.9571 41.8195L31.7665 32.66V9.39139L15.9571 0.231934ZM15.9571 33.0172L7.68318 28.2206V13.7798L15.9571 9.00869V23.424L24.2309 28.2206L15.9571 33.0172Z' fill='%23170E30'/%3e %3cpath d='M107.275 23.3727C107.275 22.9645 107.275 22.6073 107.275 22.2756C107.275 21.6377 107.021 20.311 106.766 19.7242C104.628 14.6214 96.3791 15.5144 95.5645 21.3316C94.648 28.0417 102.438 30.9248 106.613 26.2302L104.678 24.929C102.464 26.8936 98.9759 26.5619 98.2885 23.3982H106.384H107.275V23.3727ZM98.2885 21.3826C99.0268 17.9382 103.966 17.7596 104.449 21.3826H98.2885ZM58.472 16.5095C53.9914 15.7441 51.1147 19.1629 51.522 23.4492C51.9802 28.0672 57.8865 30.2614 61.0688 26.766V28.1438H63.9964V16.3309C63.9964 16.3309 61.1706 17.9638 61.0433 18.0403C61.0433 18.0403 59.7959 16.7391 58.472 16.5095ZM57.3264 25.822C53.5077 25.3883 53.5332 19.6987 57.0464 19.1119C62.469 18.1934 62.5963 26.4088 57.3264 25.822ZM126.929 25.4648C126.471 29.5981 118.197 29.3429 116.924 25.6944L119.011 24.4698C119.597 26.1537 122.881 27.1487 123.95 25.6944C125.274 23.9085 121.048 23.4747 120.055 23.092C118.91 22.6328 117.586 21.8419 117.408 20.5151C116.72 15.5655 124.765 14.9786 126.623 18.6781L124.689 19.8263C124.103 18.2954 120.157 17.479 120.284 19.6222C120.361 20.8468 123.517 21.204 124.561 21.6633C126.318 22.4287 127.132 23.4747 126.929 25.4648ZM90.5492 18.2954C87.2142 14.3918 81.3334 16.8667 80.8497 21.7908C80.3151 27.4294 86.5523 30.8993 90.5238 26.6129V28.1438H93.2987V12.1211H90.5238V18.2699L90.5492 18.2954ZM87.7998 25.7965C83.1409 26.5874 82.2499 19.7497 86.4759 19.0864C91.2366 18.3465 92.0003 25.0566 87.7998 25.7965ZM75.8599 18.2954L74.918 17.3004C70.0555 14.3408 65.0657 19.0098 66.4404 24.2402C67.4333 28.0162 72.2958 29.9808 75.3253 27.2253C75.5544 27.0212 75.6053 26.6895 75.8599 26.6129V28.1438H78.6348V12.1211H75.8599V18.2699V18.2954ZM73.1104 25.7965C68.3752 26.4854 67.7897 19.7497 71.8121 19.1119C76.7 18.321 77.311 25.2097 73.1104 25.7965ZM112.392 16.6115H109.465V28.1693H112.392V21.102L115.6 19.2394V16.3054C114.709 16.8156 112.876 17.8872 112.392 18.1679V16.6115ZM42.4335 25.3883H49.969V28.1693H39.353V13.7795H42.4335V25.3883Z' fill='%23170E30'/%3e %3c/g%3e %3cdefs%3e %3cclipPath id='clip0_1_15718'%3e %3crect width='127' height='42' fill='white'/%3e %3c/clipPath%3e %3c/defs%3e %3c/svg%3e)

My wife, Cathy, and I have been on a mission in the last couple of years to cut expenses from our monthly budget. Monthly expenses can add up quickly if you’re not careful. Life happens in ways that can throw your plans off track. Things happen that you don’t plan on can derail your plans and can wreck your budget.

That was the case for Cathy and me.

If you’re a regular reader, you know of our long battle dealing with our son’s addiction. During these years, we made some terrible decisions with our finances. The result – pretty much starting over in our mid-fifties.

We didn’t let that tear up our marriage, though it was not an easy road. One of the things that got us through is the ability to talk about things we didn’t necessarily want to talk about. That includes talking about money and finances.

We realized going through this challenging time that we didn’t have a good handle on our finances. Though my income is variable, I was making good money. Maybe you can relate. Instead of setting it aside for saving and investing, we lived and spent as if it would last forever. That, of course, meant we didn’t have much of an emergency fund.

Life is About More Than Money

There are things more important than money. However, money and finances are in the top two or three reasons on almost every list you’ll see on what causes divorce. We now make it a point to regularly review and talk about what we’re doing with our money.

Once we began to get ourselves back on track, we looked for ways to cut spending. We combed over every aspect of our cash flow to find ways to cut our monthly bills. In today’s post, we will highlight how we did it and how much we’ve saved. We’ll also talk about what we’ve learned over the years.

Cathy is the primary author. I add my two-cents worth here and there. This month (October 2019), we cut another big chunk from our expenses. It never gets old!

How We Cut Our Monthly Budget

As you’ll read in today’s post, Cathy is the detail person who tracks the spending and savings.

First things first. Though not impossible, it will be hard to cut your expenses unless you have a personal budget.

Track your living expenses from month to month to know where your money is going. Making smart decisions about money is easier if you know how much money is coming in and going out every month.

Here’s our story of what we altered our spending habits and how much our total costs went down.

Decluttering

Hello everyone. It’s Cathy, Fred’s wife. I love saving and making money. Though this first topic isn’t part of our monthly budget-cutting ideas, it did put a lot of cash in our pockets. And it was a lot easier than we thought (especially for Fred).

When Fred started his blogging campaign, I started reading the articles on saving and cutting expenses. Nothing excites me more than saving money; finding innovative ways, and ideas on how to save.

Back in the day, I loved using paper coupons (I know old school). One of my favorite things when we first married (going on 36 years), was to clip coupons out of the Sunday paper and place in my little coupon divider before heading to the grocery store. I grew up on very little. Early on, I learned how to save and be frugal.

After reading a couple of blog articles, I decided it was time to approach Fred about selling stuff we’ve had sitting around the house for years. In other words – to declutter. You have to understand. My husband hates change! He’s resisted this plea to declutter for years. To my surprise, this time, he agreed!

I almost went into shock!

The biggest shocker was he let go of over half his books. Mind you; he had four bookshelves full. We are now down to two! I wrote about our decluttering in an earlier article. I brought in $3K from selling stuff! I’m still on the bandwagon of selling items we don’t need, but it’s been slow-moving lately.

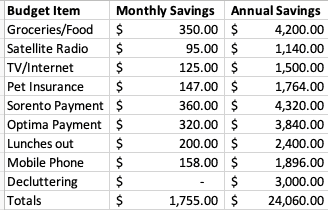

Cash made from decluttering – $3,000

Fine-Tuning the Budget

My focus has been on cutting our monthly budget. I reviewed our budget from the beginning of the year to now. I was amazed at how even the most straightforward items cut or paid off have saved. I’m sure some of you will say, it’s not rocket science, but I’m psyched about it.

Groceries

Our grocery bill here in the DMV (DC, Maryland, Virginia) is ridiculous! What a sore spot when trying to eat healthily or even gluten-free. Fred has his office at home. To get out of the house, he went out to lunch. A lot! When we looked at the budget and what he was spending, he decided to quit going out for lunch. I had already stopped going out for lunch at work, mainly to watch my food and calorie intake every day.

Lunches out (or any meal for that matter) in the DMV are expensive. We figured his eating out would average around $10/lunch. Places like Chic Fil A (one of Fred’s favorites) are less. Others are more.

Monthly budget savings – $200/mo.

Meal Planning

On Sundays, I began preparing great lunch options for both of us. That helped him with the lunches out. Here’s a quick analysis of how much we’ve cut on the grocery budget since January.

We usually plan and cook our meals for the week on Saturday and Sunday. Saturday is meal planning and list-making. We will either shop on Saturday or Sunday to get the items on our list. Meal planning has helped us save a lot of money. It cuts out most of the trips to the store to pick up extra things we forgot. That brings a surprising amount of extra savings to the budget.

We cook for the week on Sundays. We share in the weekly meal prep. Fred loves to cook in the smoker and on the grill. When he does this on Sundays, it accounts for two or three meals for the week. I cook soups, some Mexican dishes (tacos or enchilada) that accounts for a couple of meals. On nights we cook during the week, it’s usually salmon or fish that we can prepare quickly.

Food Cost Savings

For many of you reading the following numbers, you will be shocked. I’ve read accounts from other bloggers about their grocery bills. At those rates and in less expensive parts of the country, our budget could feed a family of six. Out here, it’s crazy. Your zip code matters when it comes to cost.

Sperling’s Best Places Cost of Living index for Reston Virginia is 155.5, compared to the National average cost at a 100. It’s expensive, even shopping for groceries at Trader Joes, Aldi, etc., which we do. Reston is not a cheap place to buy anything, especially housing or food.

When we looked back over our food budget for 2017, the average came in at $1,437/mo. During the first nine months of 2018, we averaged $1,087/mo.

Monthly budget savings – $350/mo.

We feel pretty darn good cutting our food budget this much. However, we’re still working on ways to slim it even lower.

2019 update – Our food costs are down to around $600/mo. Every month we look at our grocery spending and meal planning looking for ways to cut further. A great new store moved into our area. Sprouts Farmers Market is now our go-to store for almost everything. Fresh produce, which we always got at Whole Foods for the quality, we now get at Sprouts at prices significantly less than what we were paying.

We think we will likely cut our expenses down, even more, going forward.

Unnecessary Spending

Next, we looked to find other areas of overspending.

Fred loves his music. He was spending around $30/mo.buying music on iTunes. He also had subscriptions for Pandora and Spotify. (As an aside, the Spotify saved probably $20/mo. over the iTunes spending). We were even paying for Sirius XM radio in both cars. We stopped the contracts on our Sirius for a yearly savings of $780 or $65/mo.

Why do you need Sirius when you have Pandora or Spotify on your phone? Not sure where our heads were when we picked that up.

Monthly budget savings – $95/mo

FIOS vs. Alternatives

For many households, ours included, TV and mobile phone service make up a substantial monthly expense. We knew we were spending way too much for both but had the standard two-year contract to get all the bells and whistle discounts with the package. How many of us get locked into these kinds of deals?

The cable bill can really get out of hand. We rarely watch local or, for the most part, even most cable TV channels. At the end of the evening, we’ll often watch Shark Tank or a rerun of a comedy series. Mostly we spend time watching movies or a couple of favorites like This is Us or Criminal Minds. Fred, of course, watches sports.

Our Verizon TV, internet, and phone bill were around $230 a month. The package included a required home phone (which we never used or answered), high-speed internet (which I need), and the TV package. Fred did his homework to find ways to lower the costs without sacrificing what we both wanted.

He got the internet for $64.99/mo. He bought a Roku HD connection for a one-time $69.99 fee (which you don’t need if you have a Smart TV) and YouTube TV for $40/mo (now $49.95). We get everything we wanted and stopped paying for what we didn’t. We have Netflix, Amazon Prime, and numerous other options, both free and optional, paid add-ons (which we don’t use).

Our monthly bill went from an average of $230 to $105.

Monthly budget savings – $125/mo.

Pet Insurance

We have two beautiful Akitas named Titus and Kaylee. If your guessing who’s the boss, and you guessed Kaylee, you got it right. The female rules!

After three other dogs that we had to put down from old age and cancer, we decided to purchase insurance on the pups this time. The coverage was great during their younger years. The company we started with changed the coverage. It was less coverage for the same premium. Fred went to work shopping for another option.

As we get older, we pay more for insurance. It’s the same for pets. Before we switched a few years ago, we were paying around $130/mo for both dogs. When we changed to another company, our cost only went up a couple of dollars to $132, and we had much better coverage. A few years later, at renewal, it jumped to $147/mo. The reason they gave (which is always the same) was that costs and claims in our area had gone up substantially.

A $147 a month for (2) dogs, totals $1,764 a year. When we calculated their remaining life expectancy, we realized it would be more expensive paying for the insurance than saving for any significant vet bill.

After a bad experience with our last dog and cancer, we will not spend money on cancer treatment. That was a horrible experience. Nor we will run all kinds of tests on them like we did our first dog. We brought him home for five days with an IV. Fred and I slept in shifts around the clock with him on the floor. That was hard on the dogs and us. We won’t do that again. That helped us decide to drop the coverage.

Monthly budget savings – $147/mo.

Car Payments

A few years ago, we refinanced both cars at a lower rate and a much shorter payment period. I realize some reading this are questioning why we ever borrowed to buy our vehicles. Reread the first paragraph of the post for the answer.

Because the interest rate was so much lower, the shorter payment period didn’t increase the monthly payment. They went down slightly. We have now paid off both cars.

We have two Kia’s, a 2012 Sorento, and a 2011 Optima. Not sure if you know that Kia provides a 100,000-mile warranty on the drive train and engine. That warranty comes with the car. Of course, they offer an extended warranty. We declined.

We purchased a Kia Optima, and we’ve had a few problems with it. However, we have not had to pay any out of pocket on it except for tires and breaks. When we took it in for regular service, they told Fred it was out of oil. There were no oil marks in the parking place.

A week or so later, while driving to work, I heard a very noticeable clicking sound in the engine. We took it to the dealer to have it checked. The dealerships told us there was a factory defect in the piston construction of some 2011 Optima’s that caused them to burn oil. The result – a brand new engine for our Optima. Zero out of pocket dollars! We think Kia rocks!

Monthly budget savings – $680/mo. ($320 Optima, $360 Sorento)

The Cell Phone Bill

Fred here. I’ll take this section about the mobile phone bill.

Like most people, it seems, we got stuck in what seemed like a never-ending cycle of two-year contracts for our cell phones. All of the major carriers, Verizon, ATT, Sprint, and many others, want to lock you into those two- year plans.

I knew there were other options, but we couldn’t do anything until our Verizon contract expired. At long last, it expired in September 2019. I’ll let Fred take it from here.

I’d learned we could have the Verizon mobile network, which we loved and didn’t want to lose without the two-year commitment. I’d read that Total Wireless offered Verizon service with no contract. We could keep our existing phones and transfer service. Or we could buy new phones and switch the services. Our last bill from Verizon was $235. For the first time in our time with Verizon, we had additional data charges. We had a 10 gig plan and went slightly over, so it added $15 to our bill for September. Typically, our monthly bill was $218.

That’s cringe-worthy now that I know the alternatives.

The New Plan

Total Wireless offers a two-line plan for $60/mo. The plan includes unlimited nationwide talk, text, and data. The first 30 GB of data is high speed. After that, it’s at 2g speed. Our average data usage in our old plan was under 5 GB a month for both of us, except last month. We don’t stream a lot of videos on our phones. We don’t use hot spots much. It’s the perfect plan for us.

If you’re someone who needs unlimited data and full-time high speed, you can buy add on data. It’s $10 per additional 5 GB of monthly data. You can add on as many as you need. I upgraded my phone. Cathy kept hers. I found the prices for buying phones at Total Wireless were much higher. I got an iPhone XR at the Apple store. They gave me $220 on a trade-in for my iPhone 8, That’s close to what I could have sold it for on Sell Cell or one of the other online networks.

We paid for the phone. I plan on using it for years to come — no more upgrading every two years. I didn’t overspend for the phone trying to get the latest and greatest. The transition out of Verizon and into Total Wireless brought some sweet extra cash into the coffers.

Monthly budget savings – $158/mo

Back to Cathy.

Continued Budget-Cutting

Hopefully, this is just the beginning of budget-cutting for us. We review our budget together twice a month. I’m the bookkeeper of the house, that’s what I do for a living. In my day job, I help my department manage one of our many division’s budgets. It’s a budget of over $80 million. I love keeping our division on track, on time, and right on point with their budgets.

I build spreadsheets to manage these budgets. You could say I’ve become a spreadsheet geek. I’m OK with that. We used to use Mint to track and categorize our spending. We’ve since gone back to Quicken now that they have an online option. I built a spreadsheet to manage it more closely.

I recently took over managing my husband’s company’s budget. He had a basic spreadsheet. It wasn’t doing what he needed. I built a new one to better track his business.

I’m a detailed person, and part of keeping dollars on track and budget is all in the details. I point out any discrepancies or where I see we can cut dollars on spending. Most people hate that kind of detail, but not me. The more details I see, the better I like it. Bring it on. I find it challenging and rewarding. With the few savings mentioned here, so far, our budget is down $1,597 a month. I love it, but I know we can do better! Stay tuned as I research other ways to save.

Putting it all together

We were serial overspenders for years. It took a crisis in the family, much later in life than it should have, to cause us to pay closer attention to our personal finances more seriously. Here are the ingredients to be successful. Once again, these are not new concepts. They are pretty simple. As I’ve said many times, just because something is simple, it does not mean it’s easy. Here’s a summary list:

- Pay attention to personal finance and manage your money.

- Start with the basics – add your monthly income and subtract your fixed expenses.

- Create a budget using budgeting software – it will help make it much more manageable.

- Avoid overspending and credit card debt – credit card debt is a budget buster.

- Track your expenses aggressively – that’s how we cut so much from our budget.

- Look for cheaper options for the same services. Look at wants vs. needs. Focus on essentials and look at the wants you can cut.

- Spend your money wisely – avoid the impulse buys on things you think you can’t live without.

- Have money set aside for emergencies – keep the emergency fund in a savings account with easy access. That keeps the unexpected expenses off of the credit card.

- Stay on track – that takes discipline. You’ll be surprised how good it makes you feel to cut expenses and save money. The more you cut, the more you want to cut.

- Do planning and budgeting as a part of your routine.

Final thoughts

It took us a long time to get focused on our monthly expenses the way we are now. The effort has been worth it. Here are the totals for the year:

As you see, this is not a small amount of money. The declutter cash was a nice bonus. To us, it’s money that we didn’t have, and I wanted to account for it, even though the focus is on how to cut expenses drastically. These short term changes lead to long term success. In most cases, taking some simple steps (meal planning, eating out, etc.) can have a dramatic effect and help you save money – a lot of it!

You’d be amazed at what you might find in savings if you went through your budget this way. I’m sure many who are reading this are already doing most, if not all, of these things. It was an eye-opening exercise for us. I have to say; we’re pretty proud of what we’ve accomplished in the last year.

We’ve changed the way we think about budgeting. It’s made us more aware of the little things we do with our money that can add up to a high cost.

We’ve always talked about money together. Now, our conversations about money are more meaningful. Now, we constantly look for ways to save money. Rather than drudgery, as it was before, we now look at it as a fun exercise. As we said, we’re slow learners. The lesson – it’s never too late to start.

This article first appeared on the Money Mix.