'%3e %3cpath d='M15.9571 0.231934L0.147583 9.39139V32.66L15.9571 41.8195L31.7665 32.66V9.39139L15.9571 0.231934ZM15.9571 33.0172L7.68318 28.2206V13.7798L15.9571 9.00869V23.424L24.2309 28.2206L15.9571 33.0172Z' fill='%23170E30'/%3e %3cpath d='M107.275 23.3727C107.275 22.9645 107.275 22.6073 107.275 22.2756C107.275 21.6377 107.021 20.311 106.766 19.7242C104.628 14.6214 96.3791 15.5144 95.5645 21.3316C94.648 28.0417 102.438 30.9248 106.613 26.2302L104.678 24.929C102.464 26.8936 98.9759 26.5619 98.2885 23.3982H106.384H107.275V23.3727ZM98.2885 21.3826C99.0268 17.9382 103.966 17.7596 104.449 21.3826H98.2885ZM58.472 16.5095C53.9914 15.7441 51.1147 19.1629 51.522 23.4492C51.9802 28.0672 57.8865 30.2614 61.0688 26.766V28.1438H63.9964V16.3309C63.9964 16.3309 61.1706 17.9638 61.0433 18.0403C61.0433 18.0403 59.7959 16.7391 58.472 16.5095ZM57.3264 25.822C53.5077 25.3883 53.5332 19.6987 57.0464 19.1119C62.469 18.1934 62.5963 26.4088 57.3264 25.822ZM126.929 25.4648C126.471 29.5981 118.197 29.3429 116.924 25.6944L119.011 24.4698C119.597 26.1537 122.881 27.1487 123.95 25.6944C125.274 23.9085 121.048 23.4747 120.055 23.092C118.91 22.6328 117.586 21.8419 117.408 20.5151C116.72 15.5655 124.765 14.9786 126.623 18.6781L124.689 19.8263C124.103 18.2954 120.157 17.479 120.284 19.6222C120.361 20.8468 123.517 21.204 124.561 21.6633C126.318 22.4287 127.132 23.4747 126.929 25.4648ZM90.5492 18.2954C87.2142 14.3918 81.3334 16.8667 80.8497 21.7908C80.3151 27.4294 86.5523 30.8993 90.5238 26.6129V28.1438H93.2987V12.1211H90.5238V18.2699L90.5492 18.2954ZM87.7998 25.7965C83.1409 26.5874 82.2499 19.7497 86.4759 19.0864C91.2366 18.3465 92.0003 25.0566 87.7998 25.7965ZM75.8599 18.2954L74.918 17.3004C70.0555 14.3408 65.0657 19.0098 66.4404 24.2402C67.4333 28.0162 72.2958 29.9808 75.3253 27.2253C75.5544 27.0212 75.6053 26.6895 75.8599 26.6129V28.1438H78.6348V12.1211H75.8599V18.2699V18.2954ZM73.1104 25.7965C68.3752 26.4854 67.7897 19.7497 71.8121 19.1119C76.7 18.321 77.311 25.2097 73.1104 25.7965ZM112.392 16.6115H109.465V28.1693H112.392V21.102L115.6 19.2394V16.3054C114.709 16.8156 112.876 17.8872 112.392 18.1679V16.6115ZM42.4335 25.3883H49.969V28.1693H39.353V13.7795H42.4335V25.3883Z' fill='%23170E30'/%3e %3c/g%3e %3cdefs%3e %3cclipPath id='clip0_1_15718'%3e %3crect width='127' height='42' fill='white'/%3e %3c/clipPath%3e %3c/defs%3e %3c/svg%3e)

Graduating from college is supposed to be an achievement that unlocks the potential of your professional career. After receiving your diploma in May, having a college education is supposed to welcome the challenges and excitement of adulthood, the first steps toward your first real job that’ll act as the springboard to push — and excel — you beyond what one might think is possible in your ascent into adulthood.

At least that’s how it was sold, until reality hits: student loan debt and repayment.

There might be a grace period after graduating where you can still pretend that thousands and thousands of dollars of debt aren’t waiting for you, but it is — and you’re not alone. America is deep in a student debt crisis, with Americans owing about $1.5 trillion in student loans as of March 2019, a number that has doubled compared to what Americans owed just a decade ago.

With education costs climbings and workforce salaries paying less and less, student loan debt is hindering America’s youth in ways that affect them both at work and in their personal life.

From the Pew Research Center, here are the quick facts regarding America’s student debt crisis:

- Americans owed about $1.5 trillion in student loans.

- About one-third of adults under 30 have student loan debt.

- Young graduates with student loans are more likely to struggle financially than those without loans.

Shocking? Or expected?

A recent survey by LendingTree found that nearly eight of 10 Americans said their student loan debt hindered their life in some significant way like putting off opportunities to travel, change careers, and even start a family. Student loan debt has 46% of Americans regretting how much they borrowed and 46% of Americans regretting the education they pursued in college.

As for what loan borrowers are putting off, seeing new places was the most popular answer amongst respondents. Forty-four percent of respondents said student loan payments have kept them from new experiences in the last year, followed by saving for retirement (31%) and missing out on opportunities to go out with friends (30%).

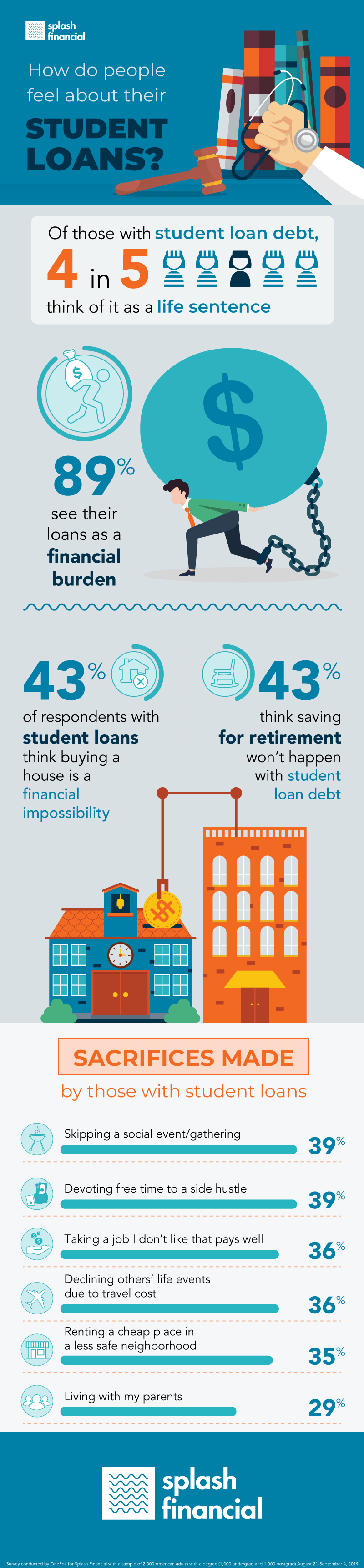

Student debt is so suffocating that four in five graduates with student loans view their debt as a life sentence, according to a separate OnePoll study that found 89% of graduates see their debt as a financial burden. This study, which polled 1,000 undergraduates and 1,000 postgraduate degree holders, found that debt holders are so bogged down with their debt that they are getting side hustles (39%), seriously budgeting (38%), and even sacrificing their career to take a job they don’t enjoy but pays well (36%).

If this sounds familiar, there are steps you can take to righting the debt ship and finding something that works for you.

The biggest mistakes borrowers can make

Shann Grewal, VP of IonTution, a company designed to help college students and alumni best manage their student loan repayment, said one of the biggest mistakes borrows can make is going on auto-pilot when the student becomes a borrower in college.

“One of the things that we stress early on is, if you’re capable of making the payment even during those periods of non-payment, go ahead and do it,” Grewal told Ladders recently. “Mitigate that interest accrual being capitalized and adding to the principal. That’s just a small tip and not everyone is in a position to do that.”

Other mistakes borrowers often make is sticking to whatever payment plan was provided to them by default. Grewal said often borrowers think the default plan is the one they should be on, and while for some it’s the sweet repayment spot, it’s often not for others with debt burden and career trajectories that aren’t going to see earning more until down the line.

Are businesses doing enough to help borrowers?

The short answer is no.

While Grewal said his clients at IonTution are “forward learning,” he said across the US, businesses aren’t doing enough to help the debt holders get a better grasp on their financial lives.

“There’s certainly a need to move faster and more decisively,” he said. “There are some good brands and employers out there that are putting together innovative programs. When they do that, I think it builds confidence among other players, specifically down market, those small and midsize businesses which tend to follow what the bigger businesses are doing. I think we’re moving in the right direction, but I think there’s a lot of work that has to be done.”

Eight percent of companies currently offer some kind of student loan repayment as a benefit in 2019, according to the Employment Benefits report by the Society for Human Resource Management. While that number doubled from the previous year (4%), it’s something on the minds of all employees with more than 50% considering student loan debt repayment an important workplace benefit, with 46% saying they’d forgo a 401(k) match to receive student loan assistance.

Grewal said he’s noticed the same pattern with his clients.

“Without a doubt. We certainly see it in our analysis. There are absolutely improvements in the effluence of recruiting if you have a repayment assistance program in place. We’re doing a lot of active measurement in terms of tenure and retention. These employees are absolutely going to stick around for along period of time, not just because of the finances, obviously, it’s clear.

“It sends a missing message that we understand that we required you to take on investment to work here and we value that investment. That creates a softer but a real rapport in the relationship between the employer and employee. They genuinely feel that the employer cares. That’s the truth — it takes a lot to go out there and do something that’s emerging, that’s not traditional, to put that program in place where you might not have the expertise in house and lean on a third party. The employers are really stepping up and I think the employees are recognizing that.”