'%3e %3cpath d='M15.9571 0.231934L0.147583 9.39139V32.66L15.9571 41.8195L31.7665 32.66V9.39139L15.9571 0.231934ZM15.9571 33.0172L7.68318 28.2206V13.7798L15.9571 9.00869V23.424L24.2309 28.2206L15.9571 33.0172Z' fill='%23170E30'/%3e %3cpath d='M107.275 23.3727C107.275 22.9645 107.275 22.6073 107.275 22.2756C107.275 21.6377 107.021 20.311 106.766 19.7242C104.628 14.6214 96.3791 15.5144 95.5645 21.3316C94.648 28.0417 102.438 30.9248 106.613 26.2302L104.678 24.929C102.464 26.8936 98.9759 26.5619 98.2885 23.3982H106.384H107.275V23.3727ZM98.2885 21.3826C99.0268 17.9382 103.966 17.7596 104.449 21.3826H98.2885ZM58.472 16.5095C53.9914 15.7441 51.1147 19.1629 51.522 23.4492C51.9802 28.0672 57.8865 30.2614 61.0688 26.766V28.1438H63.9964V16.3309C63.9964 16.3309 61.1706 17.9638 61.0433 18.0403C61.0433 18.0403 59.7959 16.7391 58.472 16.5095ZM57.3264 25.822C53.5077 25.3883 53.5332 19.6987 57.0464 19.1119C62.469 18.1934 62.5963 26.4088 57.3264 25.822ZM126.929 25.4648C126.471 29.5981 118.197 29.3429 116.924 25.6944L119.011 24.4698C119.597 26.1537 122.881 27.1487 123.95 25.6944C125.274 23.9085 121.048 23.4747 120.055 23.092C118.91 22.6328 117.586 21.8419 117.408 20.5151C116.72 15.5655 124.765 14.9786 126.623 18.6781L124.689 19.8263C124.103 18.2954 120.157 17.479 120.284 19.6222C120.361 20.8468 123.517 21.204 124.561 21.6633C126.318 22.4287 127.132 23.4747 126.929 25.4648ZM90.5492 18.2954C87.2142 14.3918 81.3334 16.8667 80.8497 21.7908C80.3151 27.4294 86.5523 30.8993 90.5238 26.6129V28.1438H93.2987V12.1211H90.5238V18.2699L90.5492 18.2954ZM87.7998 25.7965C83.1409 26.5874 82.2499 19.7497 86.4759 19.0864C91.2366 18.3465 92.0003 25.0566 87.7998 25.7965ZM75.8599 18.2954L74.918 17.3004C70.0555 14.3408 65.0657 19.0098 66.4404 24.2402C67.4333 28.0162 72.2958 29.9808 75.3253 27.2253C75.5544 27.0212 75.6053 26.6895 75.8599 26.6129V28.1438H78.6348V12.1211H75.8599V18.2699V18.2954ZM73.1104 25.7965C68.3752 26.4854 67.7897 19.7497 71.8121 19.1119C76.7 18.321 77.311 25.2097 73.1104 25.7965ZM112.392 16.6115H109.465V28.1693H112.392V21.102L115.6 19.2394V16.3054C114.709 16.8156 112.876 17.8872 112.392 18.1679V16.6115ZM42.4335 25.3883H49.969V28.1693H39.353V13.7795H42.4335V25.3883Z' fill='%23170E30'/%3e %3c/g%3e %3cdefs%3e %3cclipPath id='clip0_1_15718'%3e %3crect width='127' height='42' fill='white'/%3e %3c/clipPath%3e %3c/defs%3e %3c/svg%3e)

A new Bankrate survey will make you feel a little better about leaching off of your parents HBO GO subscription. The majority of parents reported giving their adult-children a hand with a wide range of expenses, everything from phone bills, credit card bills, student loans, and even travel costs.

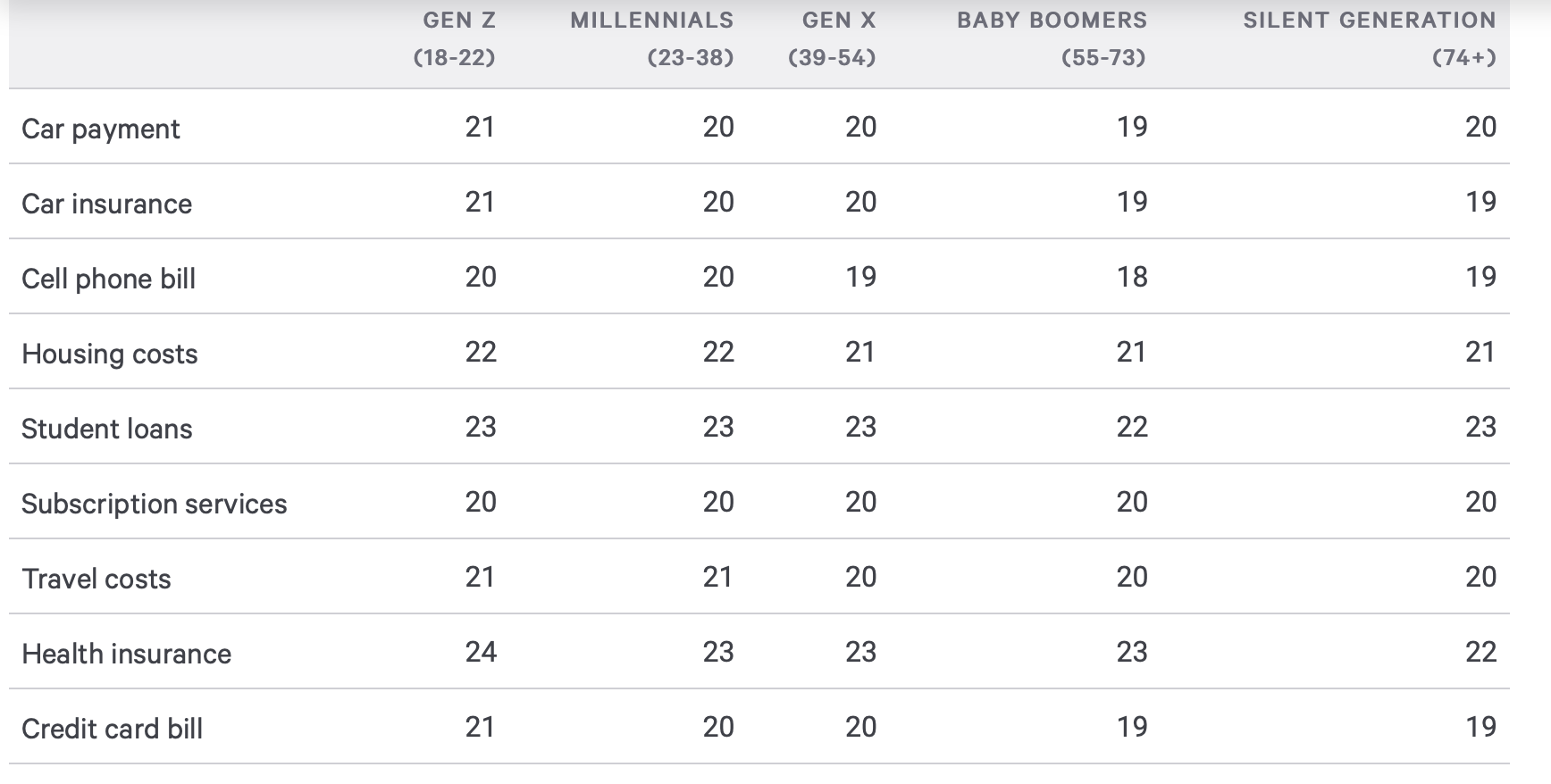

Even though Gen Zers and Millenials don’t truly feel like adults until they’ve left the nest, these generations tend to take their time doing so. The median range of assisted young adult in the study was 18 to 23. The higher the bill the more likely parents were to offer assistance, even if it met dipping into their retirement fund.

Follow Ladders on Flipboard!

Follow Ladders’ magazines on Flipboard covering Happiness, Productivity, Job Satisfaction, Neuroscience, and more!

What constitutes adulthood?

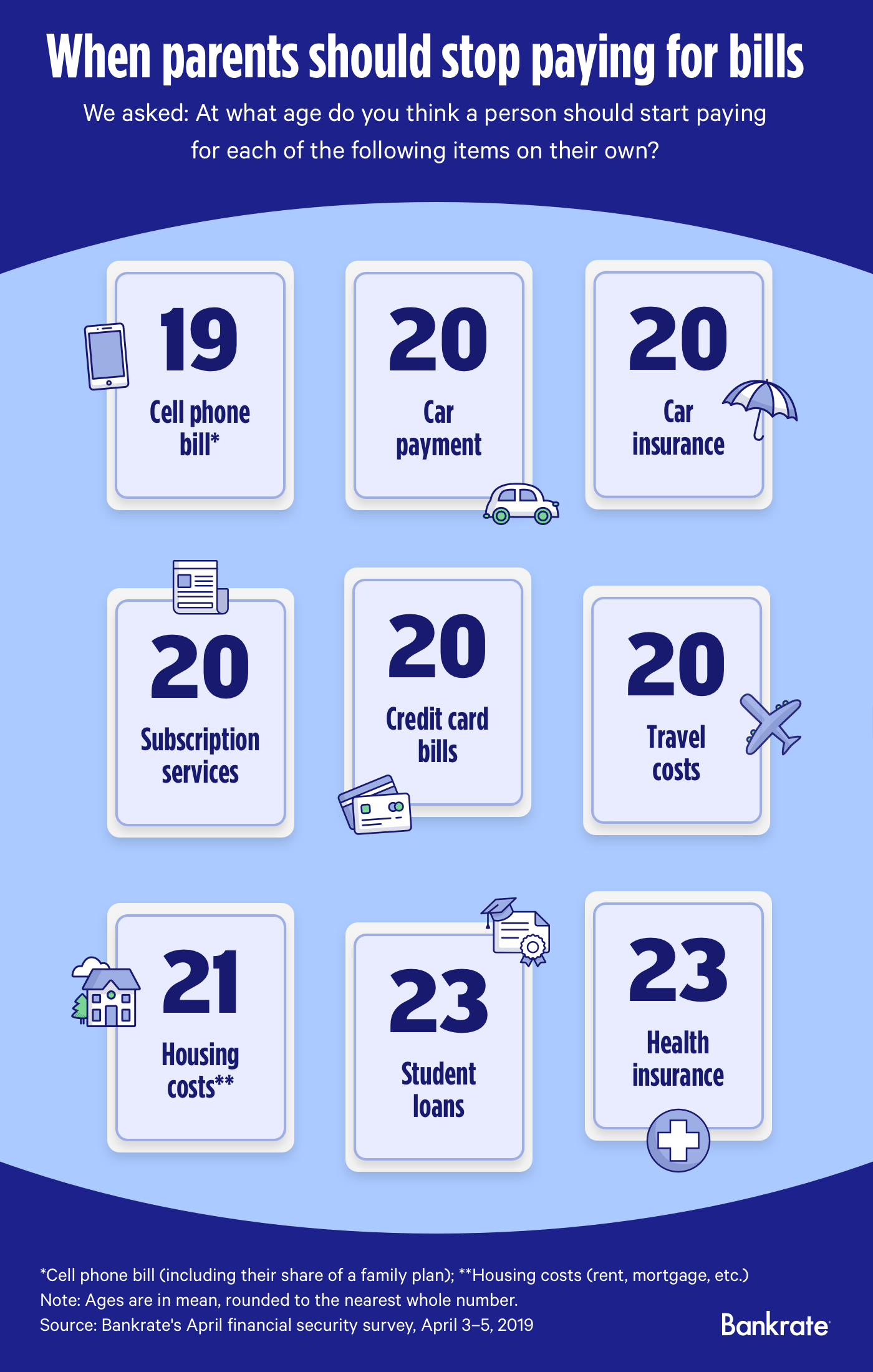

It should be clarified, just because a lot of American parents are willing to help carry some financial burdens for their children, it doesn’t mean they’re OK with their offspring’s arrested development. Most of the parents involved in the survey said that by 19-years-old, you should be paying for car payments, insurance, cell phone bills, subscription services, travel costs, and credit card bills, all on your own. To be fair, Gen Zers and Millenials, were willing to meet them in the middle, as the majority of the respondents in these generations thought that 20 years of age was closer to the mark.

Expectations seemed to vary depending on financial status. Respondents that earned an annual income under $30,000, for instance, felt that 24, was about the time their children should start paying their student loans on their own. Respondents with household incomes from 50,000 to over 80,000, felt 23 to be more appropriate.

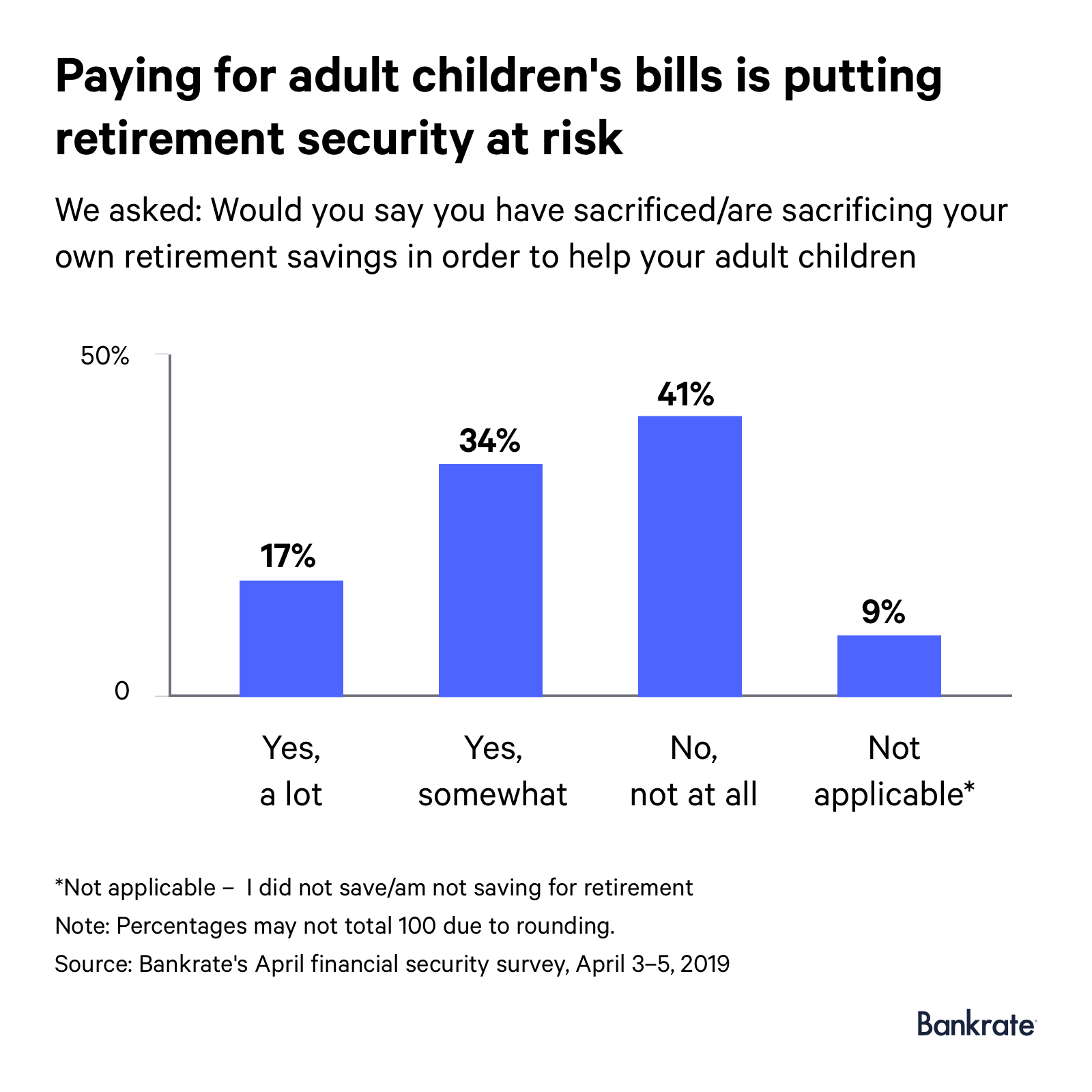

A lot of variables factored into what age individuals ought to be financially independent, but the consequences seemed to span across all the reported circumstances. Fifty percent of all the parents involved in the survey said that they are currently or already have sacrificed their retirement fund in order to keep their children afloat. One in five Americans aren’t saving for retirement, emergencies or other financial goals whatsoever, due to “not making enough money” and “large debt payments.”

Bankrate’s senior economic analyst, Mark Hamrick believes a lack of substantial wage growth and the emphasis placed on chasing higher degrees is why the assistance phenomenon has become so normalized. This causes many young Americans to enter the workforce later than they would otherwise, and when they finally do they’re saddled with an enormous amount of debt. Hamrick adds,

“This is the ironic, unintended expense of people staying in school longer. The way young people come of age has changed somewhat over the past 50 years or even longer — there’s no longer a sense of immediate need for young people to enter the workforce, even on a part-time basis.”

You might also enjoy…

- New neuroscience reveals 4 rituals that will make you happy

- Strangers know your social class in the first seven words you say, study finds

- 10 lessons from Benjamin Franklin’s daily schedule that will double your productivity

- The worst mistakes you can make in an interview, according to 12 CEOs

- 10 habits of mentally strong people