'%3e %3cpath d='M15.9571 0.231934L0.147583 9.39139V32.66L15.9571 41.8195L31.7665 32.66V9.39139L15.9571 0.231934ZM15.9571 33.0172L7.68318 28.2206V13.7798L15.9571 9.00869V23.424L24.2309 28.2206L15.9571 33.0172Z' fill='%23170E30'/%3e %3cpath d='M107.275 23.3727C107.275 22.9645 107.275 22.6073 107.275 22.2756C107.275 21.6377 107.021 20.311 106.766 19.7242C104.628 14.6214 96.3791 15.5144 95.5645 21.3316C94.648 28.0417 102.438 30.9248 106.613 26.2302L104.678 24.929C102.464 26.8936 98.9759 26.5619 98.2885 23.3982H106.384H107.275V23.3727ZM98.2885 21.3826C99.0268 17.9382 103.966 17.7596 104.449 21.3826H98.2885ZM58.472 16.5095C53.9914 15.7441 51.1147 19.1629 51.522 23.4492C51.9802 28.0672 57.8865 30.2614 61.0688 26.766V28.1438H63.9964V16.3309C63.9964 16.3309 61.1706 17.9638 61.0433 18.0403C61.0433 18.0403 59.7959 16.7391 58.472 16.5095ZM57.3264 25.822C53.5077 25.3883 53.5332 19.6987 57.0464 19.1119C62.469 18.1934 62.5963 26.4088 57.3264 25.822ZM126.929 25.4648C126.471 29.5981 118.197 29.3429 116.924 25.6944L119.011 24.4698C119.597 26.1537 122.881 27.1487 123.95 25.6944C125.274 23.9085 121.048 23.4747 120.055 23.092C118.91 22.6328 117.586 21.8419 117.408 20.5151C116.72 15.5655 124.765 14.9786 126.623 18.6781L124.689 19.8263C124.103 18.2954 120.157 17.479 120.284 19.6222C120.361 20.8468 123.517 21.204 124.561 21.6633C126.318 22.4287 127.132 23.4747 126.929 25.4648ZM90.5492 18.2954C87.2142 14.3918 81.3334 16.8667 80.8497 21.7908C80.3151 27.4294 86.5523 30.8993 90.5238 26.6129V28.1438H93.2987V12.1211H90.5238V18.2699L90.5492 18.2954ZM87.7998 25.7965C83.1409 26.5874 82.2499 19.7497 86.4759 19.0864C91.2366 18.3465 92.0003 25.0566 87.7998 25.7965ZM75.8599 18.2954L74.918 17.3004C70.0555 14.3408 65.0657 19.0098 66.4404 24.2402C67.4333 28.0162 72.2958 29.9808 75.3253 27.2253C75.5544 27.0212 75.6053 26.6895 75.8599 26.6129V28.1438H78.6348V12.1211H75.8599V18.2699V18.2954ZM73.1104 25.7965C68.3752 26.4854 67.7897 19.7497 71.8121 19.1119C76.7 18.321 77.311 25.2097 73.1104 25.7965ZM112.392 16.6115H109.465V28.1693H112.392V21.102L115.6 19.2394V16.3054C114.709 16.8156 112.876 17.8872 112.392 18.1679V16.6115ZM42.4335 25.3883H49.969V28.1693H39.353V13.7795H42.4335V25.3883Z' fill='%23170E30'/%3e %3c/g%3e %3cdefs%3e %3cclipPath id='clip0_1_15718'%3e %3crect width='127' height='42' fill='white'/%3e %3c/clipPath%3e %3c/defs%3e %3c/svg%3e)

Recently, Ladders published a bipartisan chronicle of US debt beginning with a productive row in Jefferson’s dining hall back in 1790, and ending with a grim projection from Federal Reserve Chairman Jerome Powell in November 2019:

“The federal budget is on an unsustainable path, with high and rising debt. Over time, this outlook could restrain fiscal policymakers’ willingness or ability to support economic activity during a downturn.”

Debt is officially outpacing our economy.

The problem wasn’t always suspected to be a perpetual one; it’s true but difficult to believe, I know. If you’re like me, the instant you took an interest in civics you might have also descried terms revolving around debt and debate prose to be inextricable; so much so that proposed solutions are rated by how they’re articulated much more faithfully than how they’re executed.

Commentary only seriously favored an optimistic prognosis as far as debt is concerned three times in our nation’s history. First after the compromise conceived by Jefferson, Hamilton and Madison, again during Jackson’s second term when he successfully freed America of all of its debt by selling off government lands in the west and limiting infrastructure, and for the final time just before the turn of the century following tax hikes instated by George H.W. Bush and Bill Clinton. The War of 1812 wounded the first forecast, the Panic of 1837 revealed the second to unfold more like a genie’s wish, and the great recession of 2001 made quick work of the last.

Today, the national debt sits restlessly at $22 trillion, while consumer debt is well on its way to surpassing $13 trillion. Not unlike Jackson’s initial real estate victory, the downfall of personal and consumer debt began with a series of good omens. By the early 20th century, the middle class had expanded considerably parallel to wage increases. In response to these developments, revolving credit was born which meant borrowers didn’t have to pay off their balances at the end of the month, they could just accumulate what they owed for a fee. Although many spectators blame financial illiteracy among younger generations as the primary culprit of the prolonged ballooning, Gen Zers seem to be evidencing a welcomed return to fiscal prudence.

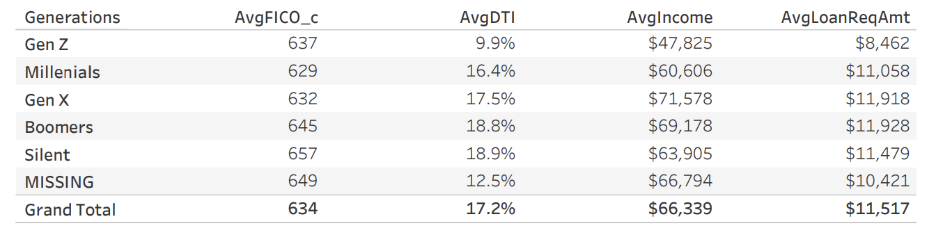

“Gen Z may be just getting into their credit-using years, but they are already showing significant differences in their credit profiles from the Millennials and GenXers that preceded them,” experts over at Lending Point explained.

“We recently analyzed just over 5 million NearPrime loan applications received between July 2018 and July 2019 to find that Gen Z, or those born after 1996, have an average FICO score that’s higher than both Millennials and Gen X. This is especially interesting when you consider that how long you’ve had credit is a key factor when it comes to credit scoring. And even with a duration of credit use playing a role in FICO scores, Gen Z is off to a strong start in building their credit profile.”

The chief reason Millennials and Generation Xers apply for personal loans is in service of debt consolidation.

Creditors are a tricky sort to negotiate with because they don’t have your best interest in mind, they have a profit in mind. There’s nothing wrong with that, but you have to become fluent in the language of fine print if you hope to make your relationship with them profitable for both parties.

If you’re not really listening, debt consolidation sounds a lot like debt elimination; if you’re not really listening lower interest rates sound like a promise, if you’re not really listening debt consolidation is indistinguishable from debt relief.

When you do away with all of the flash and glimmer of whatever pitch some third rate company tried to proselytize to you, debt consolidation is nothing more than an augmented loan with extended repayment terms. It combines all of your individual unsecured debts into one monthly bill but, in truth, just sees most applicants paying off creditors a lot longer than they would have hitherto signing their respective agreement.

Only 58% of Gen Zers occasion debt consolidation as a reason to take out a loan compared to over 74% of other generations that do so. On balance, Generation Z take out loans to cover major purchases, auto expenses, and healthcare. This generation is also borrowing in lesser amounts than Millennials and Generation X.

According to a recent LendingPoint’s report, Gen Z has an average loan amount of $8,462, which is lower than all other generations who take out a median amount between $11,000 – $11,500. This newfangled shrewdness is animated by a psychological reckoning and sins of the father. Gen Zers more than any other generation have benefited from the age of agency and accountability.

Eighty-four percent of members of this demographic surveyed said that taking charge of their finances made them feel empowered, and 74% of members belonging to this same group said they think long and hard before committing to a large expense. Lending point adds,

“It seems Gen Z doesn’t want to find themselves in the position their parents were put in during the Great Recession, and they prioritize financial stability and consider purchasing decisions. This financially conservative mindset may be the driver behind Gen Zers’ higher credit scores than both Gen X and Millennials, despite their growing interest in debt.”